Our monograph "Economics as Classical Mechanics" is under preparation.

We have compiled a draft version of Section 2.1 of Chapter 2 titled "Mechanics of Inflation and Unemployment". The interested reader may find Section 2.1 in pdf format here.

The contents:

2.1. Inflation, unemployment and labour force in the uSA

2.1.1. The (anti-) Phillips curve

2.1.2. Is labour force driving?

2.1.3. The model and data improvement

2.1.4. Forecasting inflation

2.1.5. Discussion

7/23/10

Mechanics of Gross Domestic Product

We are preparing a new monograph titled “Economics as Classical Mechanics”. This is the central part connecting two previously published monographs: “Mechanics of personal income distribution” and “Deterministic mechanics of pricing”. It is all about macroeconomics: GDP, inflation, unemployment, labor force participation rate, productivity, socialism capitalism transition. First chapater is called “Mecahnics of Gross Domestic Product”. We have prepared a draft version, which is now available here. The contents is as follows:

1.1. Real GDP per capita

1.1.1. The model

1.1.2. GDP per capita in the USA

1.1.3. Real GDP per capita Japan

1.1.4. More developed countries

1.2. Constant annual increment in real GDP per capita

1.3. Cointegration tests

1.4. Real GDP in the United States

1.5. Real GDP and S&P 500 stock market index.

We greatly appreciate any comments and criticism. The final version will likely be submitted by October 2010.

Chapter 2 (Mechanics of Inflation and Unemployment” ) is currently under initial editing and will be available for the interested readers by August 2010.

7/10/10

Deflation is approaching US

At last, deflation is approaching the US. A new post by Mark Thoma @ Economist's View:

How close to deflation are we?

Interstingly, five years ago we calculated that a deflationary period should start in 2012 and publsihed this forecast in 2006: Exact prediction of inflation in the USA.

Below is Figure 9 from this paper. ALl predcitions between 2006 and 2009 were almost absolutely correct. So, inflation has not come yet, but will visit the US soon.

How close to deflation are we?

Interstingly, five years ago we calculated that a deflationary period should start in 2012 and publsihed this forecast in 2006: Exact prediction of inflation in the USA.

Below is Figure 9 from this paper. ALl predcitions between 2006 and 2009 were almost absolutely correct. So, inflation has not come yet, but will visit the US soon.

Figure 9. Predicted inflation rate for the period between 2006 and 2016.

Several months ago we presented the same graph with actual inflation readings in this blog:Sure - disinflation continues

7/6/10

First issue of Theoretical and Practical Research in Economic Field

The first issue of TPREF (the whole journal as a pdf file ) is available now. I am an author of one article and a co-editor.

Contents: 1 | The Nexus Between Regional Growth and Technology Adoption: A Case for Club-Convergence? Stilianos Alexiadis University of Piraeus …4 | 7 | A Survey on Labor Markets Imperfections in Mexico Using a Stochastic Frontier Juan M. Villa Inter-American Development Bank … 97 |

2 | Can Shift to a Funded Pension System Affect National Saving? The Case of Iceland Mariangela Bonasia University of Naples Oreste Napolitano University of Naples … 12 | ||

3 | Global Supply Chains and the Great Trade Collapse: Guilty or Casualty? Hubert Escaith World Trade Organization … 27 | ||

4 | Some Empirical Evidence of the Euro Area Monetary Policy Antonio Forte University of Bari … 42 | ||

5 | Modeling Share Prices of Banks and Bankrupts Ivan O. Kitov Institute for the Geospheres‟ Dynamics, Russian Academy of Sciences … 59 | ||

6 | Infrastructures and Economic Performance: A Critical Comparison Across Four Approaches Gianpiero Torrisi Newcastle University … 86 | ||

7/5/10

Unemployment In Germany

Approximately a year ago we predicted the rate of unemployment, UE, in Germany at the level of 11% in 2011. This prediction was obtained from the following model linking unemployment and labor force, LF:

UE(t) = 3.2dLF(t-5)/LF(t-5) + 0.08 (1),

where the change in labor force leads the unemployment by 5 (!) years. A comprehensive discussion of the model and data, as retrieved from OECD database, is given in [1].

For this study, we borrowed unemployment estimates from the DEStatis (Federal Statistics Office). They are slightly different from those provided by the OECD, and are issued at a monthly rate.

This is time to revise the prediction and estimates. Figure 1 presents the measured and predicted unemployment rate for the period between 2002 and 2012. All in all, both curves are very close, except the most recent period.

Because of the discrepancy, we have checked the DEStatis for corroborative data on labor force and found new estimates for 2006 through 2009, which are related to national concept. When (1) is applied, one obtains the open triangle curve with the new estimates.

We still consider the level of 11% in 2011 as a reliable estimate. From 2001 to 2009 relationship (1) worked well with the estimates of labor force from the OECD.

However, there is a possibility that the new estimates of labor force are not too bad, and actual unemployment in 2011 will not be above 10%. In 2010 the rate will reach the level between 8% and 9%.

This is a good example that one can predict the future evolution of macroeconomic variables, but the past is unpredcitable. It is a common feature when statistical agencies revise their past estimates.

Figure 2. Observed and predicted rate of unemployment in Germany.

7/2/10

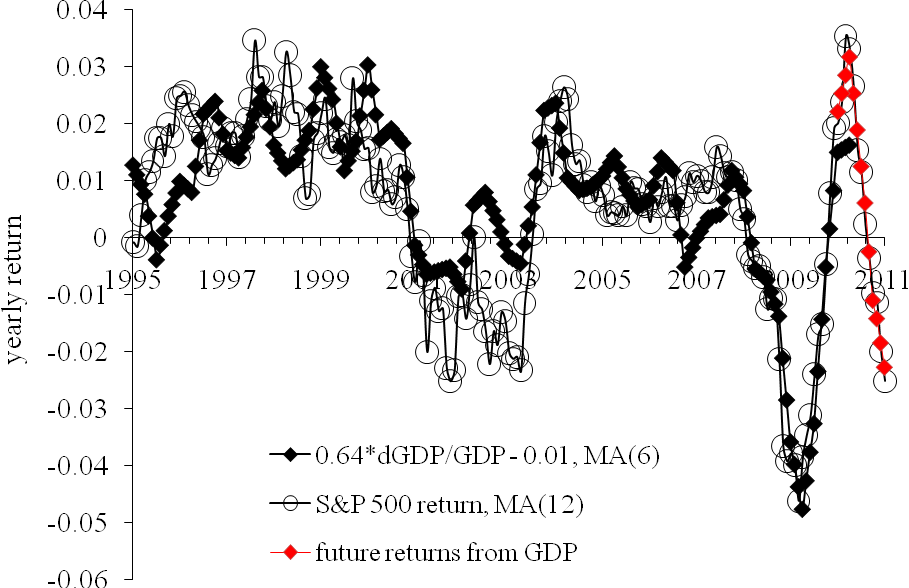

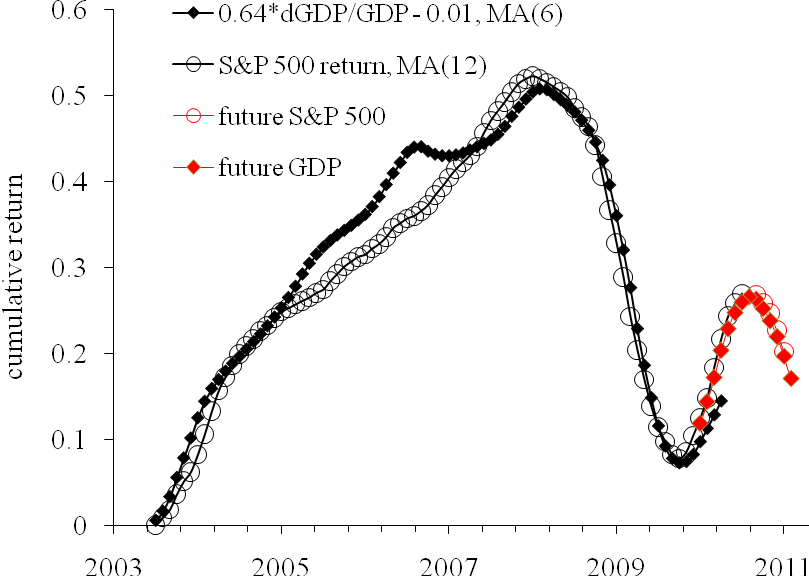

Second half of 2010 - second wave of crisis

As discussed in our working paper, there exists a trade-off between the growth rate of real GDP, G(t), and the S&P 500 returns, R(t). The predicted returns, Rp(t), can be obtained from the following relationship:

Rp(t) = 0.0062dlnG(t) - 0.01,

where G(t) is represented by (six month moving average) MA(6) of the (annualized) growth rate during six previous months or two quarters, because only quarterly readings of real GDP are available.

Figure 1 displays the observed S&P 500 returns and those obtained using real GDP, as presented by the US Bureau of Economic Analysis. The observed returns are MA(12) of the monthly returns. The period after 1996 is relatively well predicted including the increase in 2003. Therefore, it is reasonable to assume that G(t) can be used for modeling of the S&P 500 index and returns. Reciprocally, current S&P 500 may be used for the estimation of GDP.

In the previous article, we have predicted the future of S&P 500 and its returns. Now we invert the predicted figures and calculate real GDP for the same period. The bets-fit GDP figures are obtained from the cumulative curves shown in Figure 2. Our estimates from 2009Q3 to 2010Q4 are shown by red circles and red diamonds. The estimated GDP growth rates are as follows:

2009Q3: 3% (2.2%)2009Q4: 7% (5.6%)

2010Q1: 6% (2.6%)

2010Q2: +2%

2010Q3: -2%

2010Q4: -3%

In the brackets, the current estimates of the growth rate of real GDP are given, which will be all revised in July 2010. So, our model shows that GDP was slightly underestimated in the second half of 2009 and heavily underestimated in the first quarter of 2010. In 2010Q2 the growth will slow down and then a period of GDP contraction will start. Some people call it the second wave of crisis. This is what our model foresees.

Figure 1. Observed and predicted S&P 500 returns 1985 to 2011.The future S&P 500 returns are converted into GDP growth rates. Corresponding re-estimates of the returns are shown by red diamonds.

Figure 2. Cumulative observed and predicted S&P 500 returns. Red diamonds represent GDP figures which fit the predicted S&P 500 returns.

7/1/10

S&P 500 in July 2010

We continue tracking the evolution of the S&P 500 and our prediction made in the beginning of 2009 for the next six years. Since March 2009, the prediction fits the observed S&P 500 with minor deviations likely related to the emotion component of the stock market. However, the trend and its turn in May 2010 were forecasted precisely. All in all, fifteen months in a row we are right and do not see any source which may disturb our prediction for the period between June 2010 and 2014. The prediction was documented in a working paper (S&P 500 returns revisited) and several posts .

The original model links the S&P 500 annual returns, Rp(t), to the number of nine-year-olds, N9. To obtain a prediction we use the number of three-year-olds, N3, as a proxy to N9 at a six-year horizon:

Rp(t+6) = 100dlnN3(t) - 0.23

where Rp(t+6)is the S&P 500 return at a six-year horizon. Because of the properties of the N3 distribution one can replace it with linear trends for the period between 2008 and 2011, as Figure 1 shows. The model shown in Figure 1 predicts that the S&P 500 stock market index will be gradually decreasing at an average rate of 37 points per month. (Correction from the previous post where 46 points per months was used by mistake.) In June, actual closing level was 1030 (-60 relative to May 2010). This level is about 90 points below that predicted in Figure 1. This is the continuation of the May’s panic. Such dynamic "overshoot" in the beginning of a new trend is a common feature.

Figure 1. Observed S&P 500 monthly close level and the trend predicted from the number of nine-year-olds. The slope is of -37 points per month. The same but positive slope was observed between February 2009 and April 2010.

Figure 1. Observed S&P 500 monthly close level and the trend predicted from the number of nine-year-olds. The slope is of -37 points per month. The same but positive slope was observed between February 2009 and April 2010. The deviation from the new trend is a big one and one can expect the end of panic in July/August 2010. This is a nice feature of the trend. Any deviation, whatever amplitude it has, must return to the trend. So, by the past experience we may judge that 90 points should be compensated quickly. This means that the level of S&P 500 should not change much in July and August 2010. We would expect the close level between 1020 and 1050 in July 2010.

Then, the index will continue gradual decrease into 2011. Figure 2 demonstrates that the S&P 500 annual return will sink below zero in the third-fourth quarter of 2010.

Figure 2. Observed and predicted S&P 500 returns.

Figure 2. Observed and predicted S&P 500 returns.

Subscribe to:

Comments (Atom)

-

These are two biggest parts of the Former Soviet Union. To characterize them from the economic point of view we borrow data from the Tot...

These are two biggest parts of the Former Soviet Union. To characterize them from the economic point of view we borrow data from the Tot... -

These days sanctions and retaliation is a hot topic. The first round is over and we will likely observe escalation well supported by po...

-

This paper "Gender income disparity in the USA: analysis and dynamic modelling" is also of interest Abstract We analyze and deve...